7 Insider Tips for Smarter Investments in 2025

My name is Elizabeth Johnson, and I write about personal finance to help people understand complex investment concepts.

Starting to invest just $200 monthly for 40 years could earn you $86,676 more than investing $400 monthly for 20 years. This simple truth about investing remains hidden from most investors by their money managers.

My name is Elizabeth Johnson, and I write about personal finance to help people understand complex investment concepts. American households that own stocks have grown beyond 60% today, yet many still struggle with the fundamentals. A sobering reality shows that a single 1% increase in fees can reduce your returns by $146,000 over 30 years – a fact investment professionals rarely discuss.

This piece offers a detailed guide to investment basics for 2025. You’ll find seven significant insights about protecting and growing your wealth, from understanding the risk ladder to becoming skilled at diversification strategies. Let’s explore what smart money managers typically keep under wraps.

The Truth About Market Timing That Pros Won’t Admit

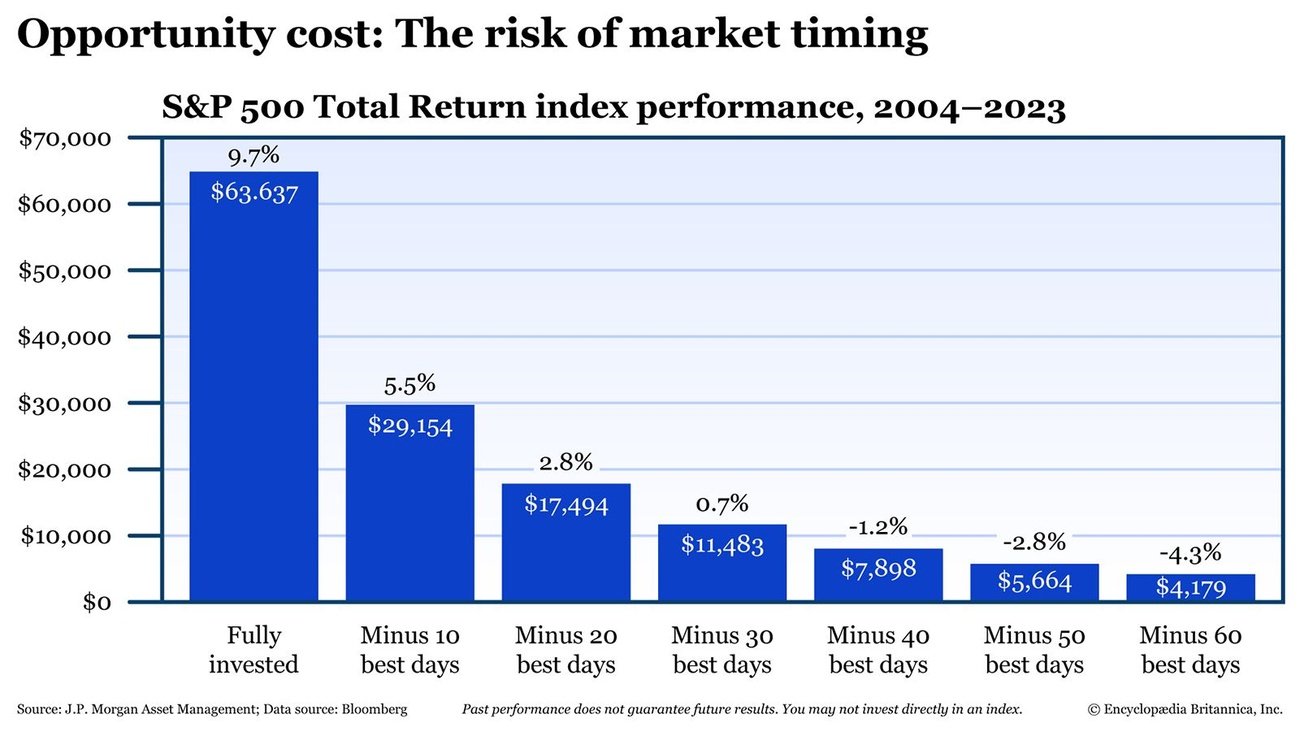

Image Source: Britannica

Market timing stands as one of the most debated topics in investment fundamentals. A landmark study by Nobel Laureate William Sharpe found that investors need to be correct 74% of the time to outperform a passive index fund [1]. All the same, the allure of perfect market timing persists.

Why Perfect Timing Is a Myth

Research shows that 78% of the stock market’s best days occur during bear markets or within the first two months of a bull market [2]. Missing just the top 10 trading days over a 30-year period could cut your returns in half [2]. More, a 2017 study revealed that funds attempting market timing underperformed other funds by 0.14 percentage points—creating a 3.8% difference over 30 years [1].

How Professionals Really Time Their Investments

Professional investors use a combination of fundamental, technical, quantitative, and economic data for market timing decisions [1]. But only 23% of actively managed funds surpassed their passive rivals over the 10-year period ending June 2019 [1]. The S&P 500 returned 45% against unanimous recession predictions from 112 professional economists [3].

The Psychology Behind Market Timing

Two key psychological factors shape market timing decisions. Hindsight bias makes investors remember their predictions as more accurate than they actually were [2]. Loss aversion causes people to weigh losses more heavily than equivalent gains [2]. These biases often lead to emotional rather than rational investment choices.

Alternative Timing Strategies for Retail Investors

Dollar-cost averaging—investing fixed amounts at regular intervals—works better than trying to time the market perfectly. A study by T. Rowe Price shows that rebalancing into stocks during market downturns improved results over subsequent years [4]. On top of that, a balanced portfolio with approximately 60% in stocks and the rest in bonds has worked better than making dramatic moves in and out of the market [5].

Hidden Costs That Eat Into Your Returns

Image Source: Breaking Into Wall Street

Small investment fees might look harmless at first glance, but they can devastate your portfolio over time. A tiny 0.50% increase in fees could eat away more than 10% of your wealth across 30 years [6].

Beyond Management Fees

Management fees get most of the attention, but other hidden costs quietly chip away at your returns. Your fund’s turnover rate shows how much of its investments get replaced yearly, creating extra transaction fees and possible tax issues [6]. Many mutual funds charge sales loads as high as 5.75% right when you buy them [6]. Even small brokerage fees add up through repeated trading and account maintenance charges [6].

Transaction Cost Analysis

The pros rely on Transaction Cost Analysis (TCA) to check how well trades execute. Investors typically pay between $1 million and $1.5 million annually in transaction costs for every $1 billion in active equity portfolios [7]. These costs mix obvious trading fees with harder-to-spot ‘market impact’ – how your trades move security prices [7]. Only about half of institutional investors say they’re happy with how clearly they can see their trading costs [7].

Tax Implications Most Managers Don’t Discuss

Taxes take a big bite out of investment returns. Higher ordinary income tax rates apply to short-term gains from assets held under a year. Long-term gains get better capital gains rates [8]. More frequent trading triggers more taxable events. Research shows active funds lose 0.75% yearly to taxes, while index funds only lose 0.30% [9].

How to Minimize Hidden Investment Costs

These strategies can help cut your hidden costs:

- Pick low-cost index funds that charge 0.20% or less [10]

- Put investments with frequent payouts in tax-efficient accounts like Roth IRAs and 401(k)s [11]

- Find brokerages that offer free trades and no maintenance fees [10]

- Let robo-advisors handle rebalancing – they usually charge about 0.25% [10]

Average expense ratios have dropped from 0.91% in 2002 to 0.37% in 2022 [11]. Smart management of these hidden costs could save you hundreds of thousands over your investing lifetime.

The Real Role of Diversification in Investment Basics

Image Source: Ashcroft Capital

Traditional portfolio theory confronts unprecedented challenges in 2025. My daily analysis of investment strategies has shown how market dynamics have moved dramatically since Harry Markowitz introduced Modern Portfolio Theory (MPT) in 1952 [12].

Why Traditional Diversification Advice Is Outdated

The conventional 60/40 portfolio allocation doesn’t deliver its previous benefits. Investors must expand beyond traditional asset classes due to bond yields at historic lows and potentially lower equity returns over the next decade [3]. Stock correlations now move close to one during market crises [12]. This undermines the basic contours of traditional diversification strategies.

Modern Portfolio Theory’s Hidden Flaws

MPT’s risk reduction approach relies heavily on historical correlation-based diversification [12]. This methodology overlooks several significant factors:

- Agency risk between fund managers and investors [12]

- Overreliance on index-based construction [12]

- Market crises’ systemic risks go unaccounted [13]

The theory assumes that returns are normally distributed, which rarely matches ground markets [13]. The 2008 financial crisis highlighted this limitation when asset class correlations increased dramatically [13].

Smart Diversification Strategies for 2025

Building resilient portfolios today requires updated approaches:

Business quality and macro factors deserve more attention than simple numerical diversification [12]. This strategy needs fewer stocks to protect against systemic risks. Alternative assets like real estate, infrastructure, and commodities serve as vital portfolio components [14]. These investments shield against inflation when traditional safe havens become scarce.

The best results come from combining core bonds for income and recession protection with inflation-sensitive real assets [14]. Note that diversification works both ways – it reduces downside exposure and upside potential equally [12].

The industry’s focus on short-term volatility instead of long-term fundamentals creates incorrect risk assessments [12]. A review of investments should focus on absolute returns rather than measure comparisons. Clients care about their total returns, not relative performance [12].

Risk Management Secrets of Top Money Managers

Image Source: Investopedia

Professional money managers use sophisticated risk management techniques that most retail investors never see. My experience as a finance blogger has helped me break down these core strategies that protect and grow wealth.

Position Sizing Techniques

Position sizing helps you decide how many units of security to buy based on your risk tolerance and account size. Most retail investors should risk no more than 2% of their investment capital on any single trade [15]. To name just one example, a $25,000 account should limit risk to $500 per trade [15]. This strategy will give a safety net where even 10 straight losses would only reduce your capital by 20% [15].

Stop-Loss Strategies That Actually Work

Stop-loss orders sell securities automatically at preset price levels. The right placement matters more than just setting them. Your position size should be cut in half before earnings announcements or in volatile markets to lower gap risk [15]. Professional traders place their stops near support and resistance levels because prices tend to reverse in these zones [16].

Portfolio Rebalancing: The Professional Way

Studies show that annual rebalancing gives the best risk-return balance [17]. A 5% threshold for rebalancing works best – you adjust when allocations move more than 5% from your targets to maintain risk levels [18]. This method works especially when you have higher transaction costs during market volatility [17].

Risk-Adjusted Return Calculations Made Simple

The Sharpe ratio remains the most common risk-adjusted return metric [19]. It shows investment returns beyond the risk-free rate for each unit of volatility [19]. Two investments might give similar returns, but the one with lower risk shows better risk-adjusted performance [19]. Higher Sharpe ratios ended up showing better risk-to-return outcomes for investors [20].

These professional risk management techniques can help protect your portfolio as you chase growth opportunities. Note that successful investing focuses on managing risk effectively rather than just chasing maximum returns. This approach leads to consistent, long-term results.

The Psychology of Successful Investing

Image Source: Jaro Education

Investor psychology shapes investment success more than market analysis alone. Studies show that emotional investing causes a staggering 50% reduction in portfolio returns over 20 years [5].

Emotional Discipline Techniques

Mindfulness practices are the foundations of emotional control during market volatility. Research shows investors who wait before making investment decisions earn better returns [21]. Dollar-cost averaging works well – you invest fixed amounts at regular intervals whatever the market conditions [22]. This strategy helps investors avoid the fear and greed cycle that causes poor timing decisions.

Behavioral Biases Money Managers Don’t Talk About

Hidden biases affect investment decisions significantly. Cognitive bias creates overconfidence, making investors believe they know more about picking stocks [23]. Confirmation bias makes investors look for information that supports their beliefs while ignoring contrary evidence [24]. Loss aversion doubles the emotional impact of losses compared to equivalent gains [23].

Decision-Making Frameworks Used by Pros

Professional investors employ systematic frameworks to avoid emotional pitfalls. The Fear and Greed Index measures market sentiment through volatility, trading volume, and technical indicators [23]. Successful frameworks also include:

- Position sizing rules that limit exposure on individual investments

- Regular portfolio reviews based on objective metrics

- Automated rebalancing strategies that maintain target allocations

Research shows that missing all but one of the top 10 market days over two decades can cut portfolio returns in half [5]. A structured decision framework helps investors maintain emotional discipline for long-term success.

These psychological aspects of investment fundamentals help investors direct through market volatility and sidestep common emotional traps. As Warren Buffett aptly noted, successful investing requires being “fearful when others are greedy and greedy when others are fearful” [25].

Alternative Investment Strategies for Beginners

Image Source: WallStreetMojo

Statistics show alternative investments grew from 6% to 12% of the global investment market between 2003 and 2018, with projections reaching 24% by 2025 [1]. My experience as a finance blogger who focuses on investment fundamentals has shown these investments create unique opportunities beyond traditional portfolios.

Beyond Stocks and Bonds

Alternative investments cover assets outside typical stock and bond markets, from commodities to private equity. The 2008 recession sparked renewed interest in these investments [26]. Family offices now dedicate an average 45% of their investment portfolios to private investments [27]. These investments provide significant portfolio diversification, particularly as stock and bond correlations become closer [28].

Real Asset Investing Fundamentals

Real assets are the foundations of economic development and offer several benefits:

- Income generation through rental yields and dividends

- Protection against potential inflation

- Lower correlation with traditional investments [29]

Real assets include commercial properties, infrastructure networks, and commodities. Their physical characteristics give them value, which often preserves long-term worth better than traditional investments [29].

Alternative Investment Risks and Returns

Risk assessment plays a vital role. Alternative investments need:

- Higher minimum investments

- Longer holding periods

- Greater risk tolerance

- More sophisticated investment knowledge [30]

These investments can be highly illiquid, which means investors might wait months or years to recover their original investment [26]. Financial experts suggest keeping less than 10% of liquid assets in alternatives [26].

Getting Started with Alternative Investments

New alternative investors should follow these strategies:

- Begin with a smaller allocation and increase it gradually over 3-5 years [27]

- Choose regulated offerings that provide better liquidity and lower investment minimums [2]

- Look into interval funds that offer quarterly or annual redemption opportunities [2]

Alternative investments should match your financial goals, risk tolerance, and time horizon. Careful selection and proper diversification can improve portfolio returns while potentially reducing overall risk [2].

The Truth About Investment Research

Image Source: Investopedia

Investment research is the life-blood of successful portfolio management, but many investors don’t realize how important it is. My ten years of analyzing market trends have shown that good research leads to better investment results.

Professional Research Methods

Institutional investors’ buy-side analysts look for promising investments that match their fund’s strategy [4]. These professionals study financial statements, economic indicators, and market trends to create detailed research reports. Investment banks’ sell-side analysts provide recommendations about buying, holding, or selling specific securities [4].

Tools and Resources the Pros Use

Professional investors employ sophisticated tools to analyze thoroughly. The Black Diamond Wealth Platform makes portfolio management easier through daily account reconciliation [31]. Riskalyze helps test portfolios under different scenarios and checks client risk tolerance [31]. AI and machine learning help analysts process big data faster and create practical insights [4].

Creating Your Own Research Framework

A strong research framework needs three key features:

- Transparency: Your framework should light up a company’s business basics and separate important information from noise [6].

- Testability: Look at facts you can verify and stay honest with yourself. Many investors only check their investment ideas through stock prices, but this doesn’t work well enough [6].

- Universality: Your framework should work for any investment chance and help you compare options. Here are the core elements to think about:

- How well it generates revenue

- The rate of turning revenue into profit

- Money spent on future growth [6]

EDGAR’s searchable database gives you access to important company filings [32]. Look at both numbers (financial statements) and quality factors (management team, competitive edges) [32]. A systematic approach to analyzing investments will help arrange each decision with your financial goals [32].

Benchmarking Overview

| Investment Basic | Challenge/Focus | Statistics/Data | Strategy/Solution | Risk/Consideration |

|---|---|---|---|---|

| Market Timing | The perfect timing myth | You need to be right 74% of the time to perform better than passive index funds | Dollar-cost averaging works better than trying to time the market | Your returns can drop by half if you miss the top 10 trading days over 30 years |

| Hidden Costs | How fees affect returns | A 0.50% increase in fees reduces wealth by 10% over 30 years | Low-cost index funds make more sense (≤0.20% expense ratio) | Active funds face 0.75% annual tax drag while index funds face only 0.30% |

| Diversification | Limitations of traditional 60/40 portfolios | Stock correlations approach 1 during market crises | Quality businesses and macro factors deserve attention | MPT assumes normal return distribution, which rarely happens in reality |

| Risk Management | The value of position sizing | A maximum 2% risk per trade works best | A 5% threshold helps in rebalancing | Your capital only drops by 20% even after 10 straight losses |

| Investment Psychology | How emotions affect investing | Emotional decisions can cut returns by 50% over 20 years | Systematic frameworks and mindfulness practices help significantly | Losses feel twice as intense as equivalent gains |

| Alternative Investments | Portfolio variety | These investments grew from 6% to 12% (2003-2018) | Begin with small amounts and increase gradually over 3-5 years | You need higher minimums and longer holding periods |

| Investment Research | Research framework value | Not specifically mentioned | Transparency, testability, and universality matter most | Both quantitative and qualitative factors need assessment |

Wrap-Up

Smart money management goes way beyond tracking market trends or chasing hot stocks. My research and experience have revealed seven simple investment principles that show how small decisions can substantially affect your long-term wealth building.

Note that you cannot perfectly time the market, and hidden fees will silently eat away at your returns. Your wealth drops by 10% over 30 years with just a 0.50% rise in fees. Today’s market realities demand updates to traditional diversification strategies. Business quality and macro factors are now significant considerations.

Professional risk management techniques, especially when you have the 2% position sizing rule, shield portfolios during market volatility. Your psychological discipline matters just as much – emotional investing slashes returns by half over 20 years. Alternative investments are projected to reach 24% of the global market by 2025 and provide unique opportunities with careful planning.

A decade of analyzing investment trends has taught me that success comes from blending these fundamentals with solid research and emotional discipline. You can learn more at my hub 👉 Zyntra.io. These simple investment principles deserve your attention one at a time. Your future self will appreciate these informed, strategic investment choices instead of blindly following conventional wisdom.

Level Up Your Knowledge with These Must-Read Blogs:

• 💰 The Best Debt-Free Strategy for Buying Big-Ticket Items

• 📦 How to Master the Envelope Method – A Simple Guide to Stress-Free Budgeting

• 🎯 How to Stick to a Budget – A Foolproof System That Works

• 📊 7 Investment Risk Types Smart Beginners Must Know in 2025

• 🚫 12 Costly Investment Mistakes Smart Investors Never Make in 2025

• 📈 13 Proven Investment Metrics to Maximize Returns in 2025

• ⚠️ 10 Costly Investment Mistakes Beginners Must Avoid Today

FAQs

Q1. What are some key investment basics that smart money managers often don’t share?

Smart money managers often don’t discuss the limitations of market timing, hidden costs that erode returns, the need to update traditional diversification strategies, professional risk management techniques, the psychology of successful investing, alternative investment opportunities, and the truth about investment research methodologies.

Q2. How important is market timing for investment success?

Perfect market timing is largely a myth. Research shows that investors need to be correct 74% of the time to outperform passive index funds. Instead of trying to time the market, most experts recommend strategies like dollar-cost averaging and maintaining a balanced portfolio over the long term.

Q3. What are some hidden costs that can impact investment returns?

Hidden costs that can significantly impact returns include fund turnover fees, sales loads, brokerage fees, and tax implications from frequent trading. Even a small increase in fees, such as 0.50%, can reduce wealth by over 10% over 30 years. Choosing low-cost index funds and being aware of these hidden costs can help maximize returns.

Q4. How should investors approach diversification in today’s market?

Traditional diversification advice, like the 60/40 portfolio, may be outdated. Modern approaches focus on business quality and macro factors rather than simple numerical diversification. Investors should consider alternative assets like real estate and commodities, and evaluate investments based on absolute returns rather than benchmark comparisons.

Q5. What role does psychology play in successful investing?

Psychology plays a crucial role in investment success. Emotional investing can lead to a 50% reduction in portfolio returns over 20 years. Successful investors often use systematic frameworks to counter emotional pitfalls, implement mindfulness practices, and maintain discipline during market volatility. Understanding and managing behavioral biases is key to long-term investment success.

References

[1] – https://inspirafinancial.com/individual/resources-education/retirement-wealth/alternative-investments-diversification-strategy

[2] – https://www.morganstanley.com/ideas/alternative-investments-portfolio-diversification

[3] – https://caia.org/blog/2021/10/14/challenging-modern-portfolio-theory

[4] – https://corporatefinanceinstitute.com/resources/capital_markets/comprehensive-guide-to-investment-research/

[5] – https://rcsplanning.com/emotional-investing/

[6] – https://www.forbes.com/sites/erikkobayashisolomon/2017/04/05/every-investor-needs-sound-framework/

[7] – https://www.bfinance.com/us/insights/transaction-cost-analysis-tca

[8] – https://usaaef.org/invest-for-the-future/investing/investing-for-growth/tax-implications-of-investing/

[9] – https://www.cordantwealth.com/4-hidden-investment-expenses-that-may-be-undermining-your-returns/

[10] – https://www.consumerreports.org/bank-fines-fees/how-to-avoid-investment-fees/

[11] – https://www.forbes.com/sites/financialfinesse/2024/04/26/minimizing-the-cost-of-investing/

[12] – https://www.moneymanagement.com.au/features/editorial/how-modern-portfolio-theory-has-failed-investors

[13] – https://www.riverbendinvestments.com/the-problem-with-modern-portfolio-theory/

[14] – https://am.jpmorgan.com/se/en/asset-management/per/insights/market-insights/investment-outlook/portfolio-diversification/

[15] – https://www.investopedia.com/terms/p/positionsizing.asp

[16] – https://www.morpher.com/blog/stop-loss-strategies

[17] – https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/tuning-frequency-for-rebalancing.html

[18] – https://www.troweprice.com/personal-investing/resources/insights/whats-the-best-approach-for-portfolio-rebalancing.html

[19] – https://www.investopedia.com/terms/r/riskadjustedreturn.asp

[20] – https://corporatefinanceinstitute.com/resources/wealth-management/risk-adjusted-return-ratios/

[21] – https://investor.vanguard.com/investor-resources-education/article/the-science-behind-money-and-emotion

[22] – https://www.investopedia.com/articles/basics/10/how-to-avoid-emotional-investing.asp

[23] – https://www.cnbc.com/select/how-to-avoid-emotional-investing/

[24] – https://www.blackrock.com/uk/professionals/solutions/mymap/the-psychology-of-investing

[25] – https://www.rothschildandco.com/en/newsroom/insights/2023/10/wm-uncovering-behavioral-biases-when-investing/

[26] – https://www.investopedia.com/how-to-buy-alternative-investments-7369694

[27] – https://privatebank.jpmorgan.com/nam/en/insights/markets-and-investing/our-guide-to-building-out-an-alternative-investment-portfolio

[28] – https://www.fidelity.com.hk/en/start-investing/learn-about-investing/multi-asset-investing/beyond-stocks-and-bonds

[29] – https://www.nuveen.com/en-us/insights/alternatives/on-solid-ground-foundations-of-real-assets-investing

[30] – https://www.jpmorgan.com/insights/investing/investment-strategy/the-case-for-alternative-investments

[31] – https://www.investopedia.com/articles/financial-advisors/050715/10-best-tools-financial-advisors.asp

[32] – https://www.nerdwallet.com/article/investing/how-to-research-stocks

Visit Zyntra.io for More Insights 🚀

Elizabeth Johnson is an award-winning journalist and researcher with over 12 years of experience covering technology, business, finance, health, sustainability, and AI. With a strong background in data-driven storytelling and investigative research, she delivers insightful, well-researched, and engaging content. Her work has been featured in top publications, earning her recognition for accuracy, depth, and thought leadership in multiple industries.